2026 Startup DPIIT Notification: What Has Changed For Startups Since 2019

- Saswata Tewari

- May 21

- 4 min read

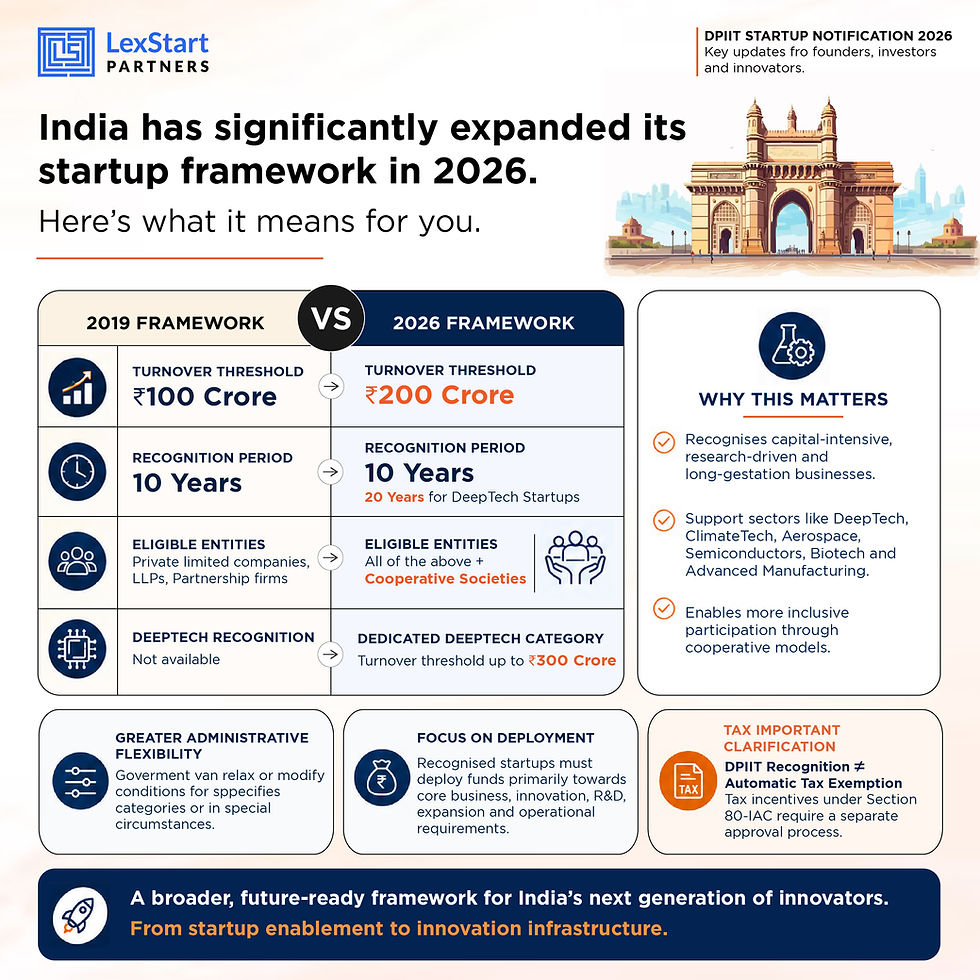

On 4 February 2026, the Ministry of Commerce and Industry notified the revised startup framework through G.S.R. 108 (E)[1] (“2026 Notification”), marking an important development in India’s startup regulatory landscape. The 2026 Notification updates the recognition architecture that had been previously been governed under G.S.R. 127 (E)[2], dated 19 February 2019 (“2019 Framework”).

The 2019 Framework was designed for a startup ecosystem that was still relatively early in its development and primarily reflected conventional technology and innovation led businesses. By 2026, however, the revised notification acknowledges a wider range of business models, including those that are more capital-intensive, research-driven, or linked to long development cycles and infrastructure-heavy operations.

Expanded Eligibility and Higher Thresholds for StartUps

Under the 2019 Framework, startup recognition was limited only to private limited companies, limited liability partnerships, and registered partnership firms[3]. However, the 2026 Notification now extends eligibility to multi-state cooperative societies registered under the Multi-State Cooperative Societies Act, 2002, as well as cooperative societies registered under applicable State or Union Territory Cooperative Societies Act with the respective Registrar of Cooperative Societies in India[4].

This is a meaningful policy development because it broadens the startup recognition framework beyond traditional venture-backed corporate structures. Community-led enterprises, agricultural innovation platforms, rural technology initiatives, and cooperative-driven commercial models may now potentially access the benefits of the Startup India regime.

The turnover threshold has also been revised upward. A startup may continue to qualify for recognition provided its turnover has not exceeded INR 200 crores in any financial year since incorporation or registration[5], as compared to the earlier INR 100 crore threshold under the 2019 Framework.

The age limit for startups continue to remain 10 years from incorporation or registration[6].

Deep Tech StartUps Receive Dedicated Recognition

An important feature of the 2026 Notification is the introduction of a dedicated sub-category for “Deep Tech Startups” within the broader startup recognition framework.

The 2026 Notification defines a “Deep Tech Startup” as a startup engaged in the business of building solutions based on novel scientific or engineering advancements, involving substantial research and development funding, significant novel intellectual property, and extended commercialization timelines accompanied by technological or scientific uncertainty[7].

For entities recognised as Deep Tech Startups, the permissible recognition period has been identified as 20 years from incorporation or registration[8], while the turnover threshold has been capped to INR 300 crores[9].

The policy rationale underlying this distinction is commercially intuitive. Deep tech ventures often require sustained investment in research, prototyping, validation, testing, regulatory approvals, and eventual commercialization. In sectors such as semiconductors, biotechnology, climate technology, aerospace, advanced manufacturing, and industrial engineering, commercial maturity frequently occurs over significantly longer periods than those associated with conventional software startups.

The 2019 Framework was therefore not always well suited to these business models. By extending both, the recognition period and turnover cap, the 2026 Notification signals a deliberate policy shift toward supporting long-gestation innovation ecosystems.

However, deep tech classification is not automatic. The notification expressly provides that determination of whether an entity satisfies the characteristics of a Deep Tech Startup will be assessed by the Department for Promotion of Industry and Internal Trade (“DPIIT”) in accordance with separately prescribed frameworks, parameters, and guidelines, based on documentation and disclosures submitted by the applicant[10].

Administrative Flexibility and Regulatory Discretion

The 2026 Notification also introduces greater administrative flexibility within the recognition process:

The revised framework additionally incorporates relaxations and modifications mechanism enabling the Central Government to relax or modify one or more conditions for specified categories of startups or in individual cases involving special circumstances. While this should not be interpreted as an unrestricted exemption power, it nevertheless introduces a level of policy flexibility that was comparatively limited under the earlier framework[11].

Recognised startups (including deep tech startups) are mandated to deploy funds primarily toward core business operations, innovation, research, expansion, and operational requirements[12].

The 2026 Notification further restricts investment by start-ups, including a deep tech startups in specified non-core assets and activities, including certain residential real estate, luxury assets, speculative activities, jewellery, and passive investments, except where such assets form part of ordinary business operations. These restrictions appear intended to preserve the policy rationale underlying the start-up recognition framework by ensuring that regulatory benefits remain linked to genuine entrepreneurial and innovation-oriented activity rather than passive investment structures[13].

Recognition and Tax Benefits Continue to Remain Distinct

The 2026 Notification does not alter the long-standing distinction between DPIIT recognition and eligibility for tax benefits under Section 80-IAC of the Income Tax Act, 1961.

A common misconception within the startup ecosystem is that DPIIT recognition automatically confers tax exemption benefits. In practice, recognition merely functions as the threshold qualification. Eligible startups seeking tax incentives under Section 80-IAC must continue to undergo a separate certification process before the Inter-Ministerial Board in the prescribed manner[14].

Conclusion

The Startup India Initiative[15], launched in January 2016, sets the policy foundation for India’s startup ecosystem by creating a formal framework to encourage innovation, entrepreneurship, and scalable business models. The 2019 Framework translated that policy objective into a more structure eligibility regime, but over time it became clear that the original thresholds were not fully aligned with the realities of capital intensive and research-driven businesses.

The 2026 Notification marks the next stage in that evolution since it broadens eligibility, formally recognises deep tech startups, and introduces greater flexibility while preserving the core principle that regulatory benefits should remain tied to genuine innovation.

[1] Ministry of Commerce & Industry, G.S.R. 108 (E) (Feb. 4, 2026) (India)

[2] Ministry of Commerce & Industry, G.S.R.127 (E) (Feb. 19, 2019) (India)

[3] Id. §1(a) (i)

[4] G.S.R 108 (E), supra note 1, §1(a)(i)

[5] G.S.R 108 (E), supra note 1, §1(a)(iii)

[6] G.S.R 108 (E), supra note 1, Id. §1(a)(ii)

[7] G.S.R 108 (E), supra note 1, §1(n)

[8] G.S.R 108 (E), supra note 1, proviso (a) to §1(a)

[9] G.S.R 108 (E), supra note 1, proviso (b) to §1(a)

[10] G.S.R 108 (E), second proviso to §1(n) (iv)

[11] G.S.R 108 (E), Id. §7

[12] G.S.R 108 (E), Id. §4

[13] G.S.R 108 (E), Id. §5

[14] G.S.R 108 (E), Id. §3

[15] Startup India Initiative, Ministry of Commerce & Industry, launched on Jan. 16, 2016 [https://www.startupindia.gov.in/content/sih/en/about-startup-india-initiative.html] (last visited on May 13, 2026).

Comments